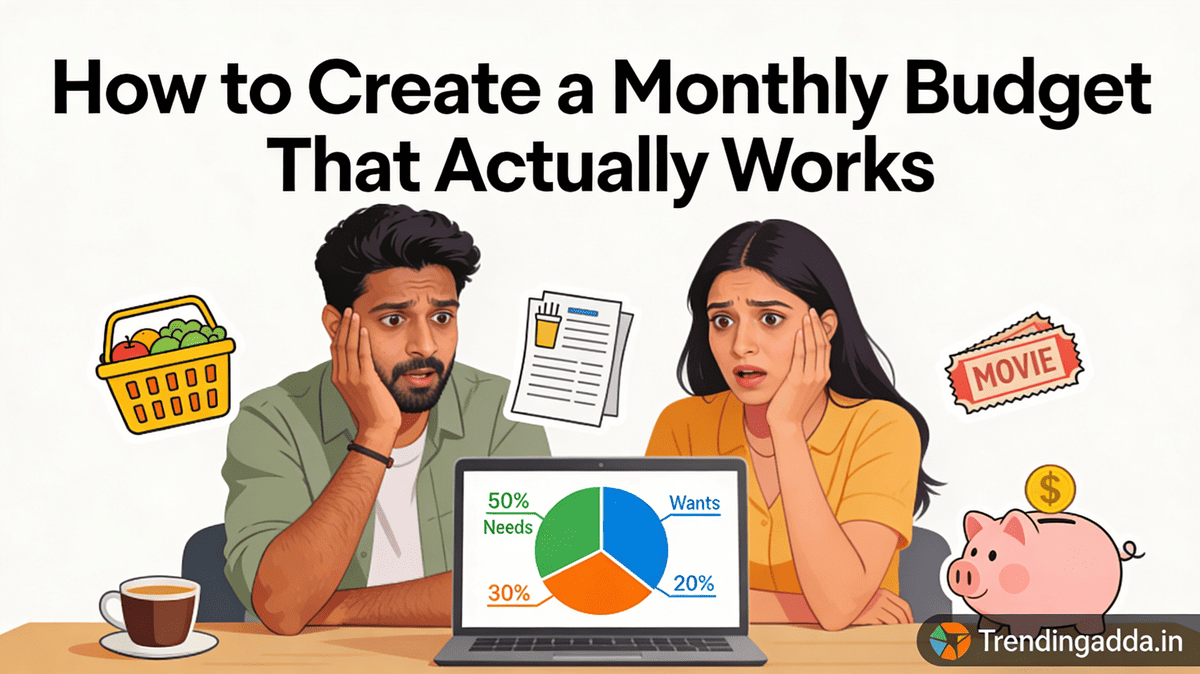

Creating a monthly budget sounds simple, but in real life, most budgets fail within the first few weeks. The reason is not lack of income—it is lack of a realistic system. A budget that actually works is flexible, practical, and designed for real Indian lifestyles.

This complete guide will help you understand how to create a monthly budget that actually works, even if you have a low salary, irregular income, family responsibilities, or past failures with budgeting.

Why Most Monthly Budgets Fail (The Hard Truth)

Before learning how to build a working budget, you must understand why most people fail.

Common Reasons Budgeting Fails in India

- Unrealistic expense limits

- Ignoring festivals, weddings, and emergencies

- Not tracking small daily expenses

- Depending only on willpower

- Copying foreign budgeting rules blindly

A budget fails not because you are bad with money, but because the system is wrong.

What Is a Monthly Budget?

A monthly budget is a money plan that tells your income where to go before you spend it. It divides your salary into:

- Essentials (needs)

- Lifestyle expenses (wants)

- Savings and investments

If you don’t control your money, your money will control you.

Step 1: Know Your Real Monthly Income

Start with your actual take-home income, not CTC.

Include:

- Salary after tax

- Side income

- Freelance income (average)

Exclude:

- Bonuses (treat as extra)

- Irregular income

Indian Example: Rohit earns ₹35,000 salary + ₹3,000 side income. His budget income = ₹38,000, not CTC.

Step 2: List Your Essential Expenses First

Essentials are expenses you cannot avoid.

Essential Expenses in India

- Rent / Home EMI

- Groceries

- Electricity & water bills

- Mobile & internet

- Transport

- School fees

- Medicines & insurance

If essentials are not covered, no budget will ever work.

Step 3: Track Where Your Money Actually Goes

For one full month, track every rupee.

Daily Expenses That Destroy Budgets

- Tea & snacks

- Online food orders

- Auto/cab rides

- Impulse shopping

Real-Life Example: Priya thought she spent ₹2,000 on food outside. Tracking showed ₹4,800.

What gets measured gets controlled.

Step 4: Use a Simple Budget Rule (Indian-Friendly)

Instead of rigid foreign rules, use a flexible Indian model.

The 50–30–20 Rule (Modified for India)

- 50–55% Needs

- 25–30% Wants

- 15–20% Savings

If salary is low, even 5–10% savings is powerful.

Step 5: Create Your Monthly Budget Table

Sample Monthly Budget (₹30,000 Salary)

| Category | Amount (₹) |

|---|---|

| Rent | 8,000 |

| Groceries | 4,000 |

| Transport | 2,000 |

| Bills | 1,500 |

| Lifestyle | 4,000 |

| Savings | 3,500 |

| Emergency Fund | 2,000 |

| Buffer | 5,000 |

Always keep a buffer. Life is unpredictable.

Step 6: Pay Yourself First (The Golden Rule)

Savings should happen before spending, not after.

How to Do It

- Auto-transfer savings on salary day

- Separate savings account

What you save first, you never miss.

Step 7: Make Your Budget Flexible

A budget should bend, not break.

Flexible Budget Tips

- Increase lifestyle budget occasionally

- Adjust during festivals

- Rebalance monthly

A strict budget breaks. A flexible budget survives.

Monthly Budget Calculator Table (India)

📌 Step 1: Enter Your Monthly Income

👉 Net salary (after tax): ₹________

📊 Monthly Budget Calculator (Editable)

| Category | Percentage | Amount (₹) |

|---|---|---|

| Needs (Rent, Food, Bills) | 50–55% | ₹ ______ |

| Wants (Lifestyle, Fun) | 25–30% | ₹ ______ |

| Savings & Investments | 15–20% | ₹ ______ |

| Emergency Fund | 5–10% | ₹ ______ |

| Buffer / Miscellaneous | 5% | ₹ ______ |

| Total | 100% | ₹ ______ |

✅ Buffer is important for Indian expenses like festivals, guests, medical, repairs.

🧮 Example Budget Calculation (₹30,000 Salary)

| Category | Percentage | Amount (₹) |

|---|---|---|

| Needs | 52% | ₹15,600 |

| Wants | 25% | ₹7,500 |

| Savings | 13% | ₹3,900 |

| Emergency Fund | 7% | ₹2,100 |

| Buffer | 3% | ₹900 |

| Total | 100% | ₹30,000 |

🧮 Low Salary Budget Example (₹18,000 Salary)

| Category | Amount (₹) |

|---|---|

| Needs | ₹10,000 |

| Wants | ₹3,000 |

| Savings | ₹2,000 |

| Emergency Fund | ₹1,000 |

| Buffer | ₹2,000 |

| Total | ₹18,000 |

Yearly Budget Planner Table (India-Friendly)

| Month | Income (₹) | Needs (₹) | Wants (₹) | Savings (₹) | Emergency Fund (₹) | Buffer / Misc (₹) | Total Expenses (₹) | Surplus / Deficit (₹) |

|---|---|---|---|---|---|---|---|---|

| January | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 900 | 29,900 | +100 |

| February | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 900 | 29,900 | +100 |

| March | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 900 | 29,900 | +100 |

| April | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 2,000* | 31,100 | -1,100* |

| May | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 900 | 29,900 | +100 |

| June | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 900 | 29,900 | +100 |

| July | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 900 | 29,900 | +100 |

| August | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 2,000* | 31,100 | -1,100* |

| September | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 900 | 29,900 | +100 |

| October | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 2,000* | 31,100 | -1,100* |

| November | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 900 | 29,900 | +100 |

| December | 30,000 | 15,600 | 7,500 | 3,900 | 2,100 | 2,000* | 31,100 | -1,100* |

Note: Buffer is increased in festival months (April, August, October, December) to cover gifts, travel, weddings, and festivals.

⚡ How to Use Yearly Budget Planner

- Enter actual income for each month.

- Adjust needs, wants, savings according to seasonal changes.

- Allocate extra buffer for festivals or unexpected expenses.

- Check surplus/deficit monthly — helps to plan side income or cut costs.

- Update emergency fund monthly until target is reached.

Indian Real-Life Example: Budget on Low Salary

Amit (Age 26, Office Assistant, ₹18,000 salary)

- Saved ₹1,000 monthly

- Reduced outside food

- Built emergency fund in 1 year

Low income is not an excuse. No plan is.

Common Budgeting Mistakes to Avoid

- No emergency fund

- Ignoring irregular expenses

- Overestimating discipline

- No tracking

Budgeting for Families vs Singles

Singles

- Focus on savings & skill growth

Families

- Higher emergency fund

- Education & medical buffer

Budgeting Tools You Can Use

- Excel / Google Sheets

- Notes app

- Budget apps

- Plain diary

Tool doesn’t matter. Consistency does.

How Long Before a Budget Starts Working?

Usually 2–3 months.

First month = awareness Second month = adjustment Third month = control

How to Fix a Budget That Is Failing

- Reduce lifestyle slowly

- Increase income

- Re-check essentials

- Add buffer

Psychology of Budgeting

People fail because budgeting feels restrictive.

Budgeting is not punishment. It is permission to spend wisely.

Budget vs Saving vs Investing

- Budget = plan

- Saving = protection

- Investing = growth

All three are necessary.

Monthly Budget Checklist

- Know income

- Track expenses

- Set limits

- Automate savings

- Review monthly

Final Thoughts

A monthly budget that actually works is not perfect—it is practical.

Start small. Stay consistent. Improve monthly.

You don’t need more money. You need a better system.

Disclaimer

This article is for educational purposes only and should not be considered financial or investment advice. Readers should consult a qualified financial advisor before making any financial decisions. TrendingAdda.in is not responsible for any financial loss arising from using this information.