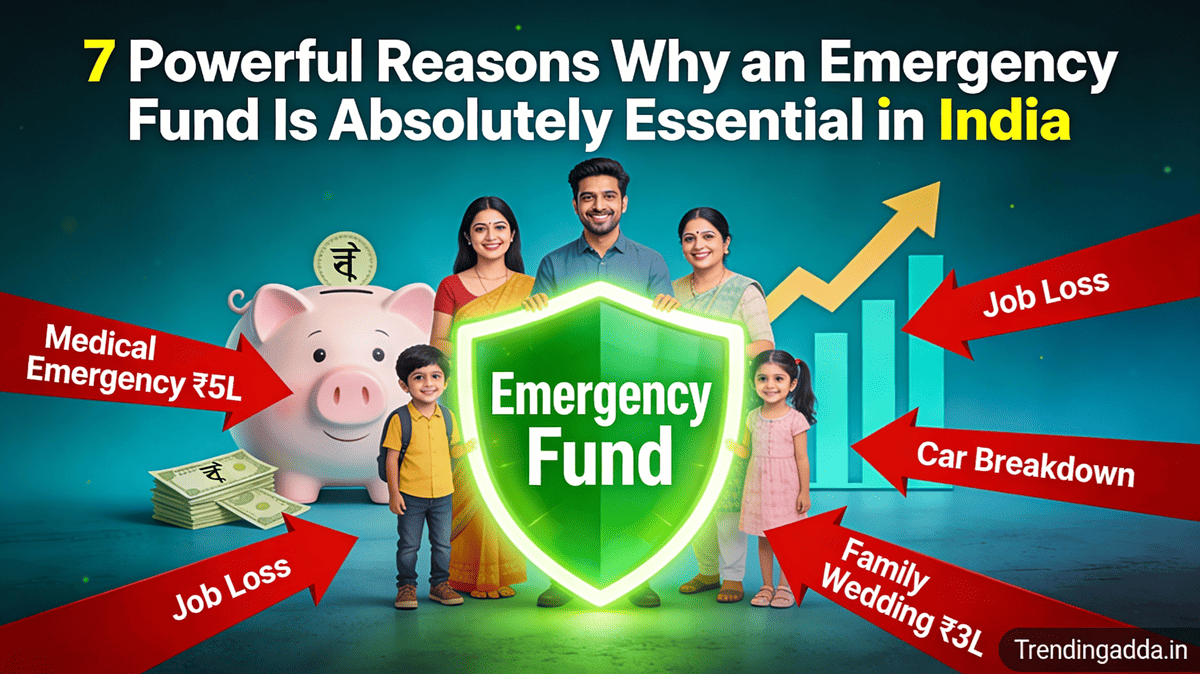

An emergency never comes with an appointment. A medical issue, job loss, salary delay, or family responsibility can hit anytime. In such moments, an emergency fund becomes the difference between calm decision-making and financial panic.

In India, many people ignore emergency savings and depend on credit cards, loans, or relatives when trouble strikes. This guide explains what it is, how much you really need, how to calculate it, where to keep it, and how ordinary Indians successfully build it—even on low salaries.

What Is an Emergency Fund?

An emergency fund is money set aside only for unexpected and unavoidable expenses. It is not for shopping, vacations, or lifestyle upgrades.

Common Emergencies in India

- Medical emergencies

- Job loss or salary delay

- Sudden house repair

- Family emergencies

An emergency fund is not an investment. It is financial insurance.

Why an Emergency Fund Is More Important Than Investments

Many people rush into investing without basic savings.

Real-Life Example

Amit (Age 29, Pune) invested aggressively in stocks but had no emergency fund. When his company delayed salaries for two months, he was forced to sell investments at a loss.

It protects your investments from emergencies.

How Much Do You Really Need?

The standard rule is 3–6 months of essential expenses. But the exact amount depends on your income stability, family responsibility, and job type.

General Rule

- Stable job, single income → 3–4 months

- Private job, dependents → 6 months

- Freelancers/business owners → 6–9 months

More uncertainty = Bigger emergency fund.

Emergency Fund Calculator Table (India-Focused)

| Monthly Essential Expenses | 3 Months Fund | 6 Months Fund | 9 Months Fund |

|---|---|---|---|

| ₹15,000 | ₹45,000 | ₹90,000 | ₹1,35,000 |

| ₹20,000 | ₹60,000 | ₹1,20,000 | ₹1,80,000 |

| ₹30,000 | ₹90,000 | ₹1,80,000 | ₹2,70,000 |

| ₹40,000 | ₹1,20,000 | ₹2,40,000 | ₹3,60,000 |

👉 Include only essential expenses like rent, food, travel, EMIs, and medicines.

Indian Real-Life Example: Low Salary Emergency Fund

Case 1: Office Assistant

Rakesh (Age 27, Delhi) earns ₹18,000/month.

- Started saving ₹1,000/month

- Built ₹12,000 in one year

- Used it during medical emergency without borrowing

Emergency fund is built with discipline, not salary size.

Case 2: Private Job with Family Responsibility

Sunita (Age 34, Jaipur) earns ₹35,000/month and supports parents.

- Target: 6 months emergency fund

- Saved via RD + savings account

- Reached ₹2 lakh in 3 years

What Expenses to Include in Emergency Fund Calculation

Include:

- Rent/house EMI

- Groceries

- Electricity & mobile bills

- Transport

- Medicines & insurance premiums

Exclude:

- Shopping

- Travel

- Entertainment

Emergency fund covers survival, not lifestyle.

Where Should You Keep Your Emergency Fund?

Accessibility is more important than returns.

Best Options in India

- Savings account

- Liquid mutual funds

- Fixed deposits with instant withdrawal

Avoid:

- Stocks

- Long-term mutual funds

- Real estate

How to Build an Emergency Fund Step by Step

Step 1: Start Small

Save ₹500–₹1,000 monthly if income is low.

Step 2: Automate Savings

Use auto-transfer after salary credit.

Step 3: Increase Gradually

Increase savings with every salary hike.

Consistency beats speed.

Emergency Fund vs Insurance: Know the Difference

Insurance covers big risks. Emergency fund covers immediate expenses.

Insurance pays later. Emergency fund pays now.

Both are necessary.

Common Mistakes People Make

- Using emergency fund for shopping

- Investing emergency fund for higher returns

- Not refilling after use

An empty emergency fund is a silent risk.

Psychology Behind Emergency Funds

People avoid emergency funds because:

- Emergencies feel distant

- Saving feels boring

Preparedness feels boring—until it saves you.

What to Do After Using Your Emergency Fund

- Rebuild immediately

- Review fund size

- Adjust monthly savings

For Different Life Stages

Single Professionals

3–4 months expenses

Married with Dependents

6 months expenses

Freelancers & Business Owners

6–9 months expenses

Emergency Fund Checklist

- Calculate monthly essentials

- Decide fund size

- Choose safe storage

- Automate savings

- Review annually

Final Thoughts

An emergency fund does not make you rich—but it keeps you safe.

Wealth grows with investing, but peace comes from preparedness.

Start today, even if the amount feels small. Your future self will thank you.

What is an emergency fund and why is it important?

An emergency fund is money saved for unexpected expenses like medical emergencies, job loss, or salary delays. It protects you from debt and financial stress during crises.

How much emergency fund should I have in India?

Ideally, you should save 3–6 months of essential expenses. If you have dependents or an unstable job, aim for 6–9 months of expenses.

Is an emergency fund more important than investing?

Yes. An emergency fund should be built before investing. Without it, you may be forced to sell investments at a loss during emergencies.

Where should I keep my emergency fund?

Keep your emergency fund in safe and liquid options like a savings account, liquid mutual fund, or instant-withdrawal fixed deposit.

Can I build an emergency fund with a low salary?

Yes. Even saving ₹500–₹1,000 per month consistently can help you build an emergency fund over time.

Should I use credit cards instead of an emergency fund?

No. Credit cards create debt and interest burden. An emergency fund gives debt-free financial security.

How often should I review my emergency fund?

You should review your emergency fund once every year or whenever your income, expenses, or family responsibilities change.

What expenses should an emergency fund cover?

It should cover essential expenses like rent/EMI, food, electricity, transport, medicines, and insurance premiums—not lifestyle expenses.

What happens if I don’t have an emergency fund?

Without an emergency fund, even one crisis can lead to loans, credit card debt, stress, and long-term financial damage.

Preparedness feels boring—until it saves you.

Disclaimer:

The information provided in this article is for educational and informational purposes only. It should not be considered financial, investment, or legal advice. TrendingAdda.in is not a SEBI-registered financial advisory platform. Readers are advised to consult a qualified financial advisor before making any financial decisions. The website will not be responsible for any financial loss incurred based on this information.